Enterprise Week

- Lily Newman

- Feb 4, 2019

- 5 min read

I regretted not being able to go to Digital Week last year so I really wanted to make sure I went too as many as I could this time round. I only had two days free during the week as I was away for the rest of the week but luckily the ones that I felt were most beneficial to me were the ones on Monday and Tuesday.

The first session I wanted to go to was 'How to become Self-Employed' first thing on Monday morning. I drove all the way down in the morning to turn up and get told the person was off ill so they had to cancel it. They did rearrange the session for Thursday but I was away so I was unable to make it but Becky from the careers office sent me the powerpoint from the session.

The powerpoint gave 12 steps to think about becoming self employed before you actually decide to become self employed.

1. Sit down and write the pros and cons of being your own boss.

2. List areas where you need to improve, for example, financial management

3. Think about your creative skills and list how they could be turned into a product or service

4. Profile your ideal customer, is it businesses or individuals. Then contact them...

5. Research into the different legal structures and understand whites best for you.

6. Consider the benefits of having a business name, against using your own name.

7. Develop a ten step plan to promote your brand

8. Contact Patlib Plymouth to discuss any potential IP issues you may have.

9. Speak to Paul (Enterprise Advisor) about creating a cashflow forecast.

10. Think about your own time management skills, how can you improve this?

11. Find a creative network to join and identify people/businesses you want to learn from.

12. Contact 10 people a week you want to work with, sell to and partner with.

I am going to sit through these questions and thoughts at later date and think a lot about them.

Pricing your work and working out hourly rate

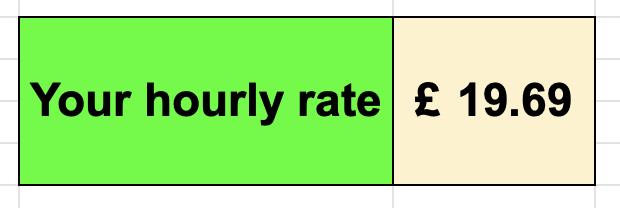

I travelled down again on Tuesday in the hope that this session hadn't been cancelled as I really wanted to go to this one as it's something that I've always thought about. The session wasn't a session where you hot spoken at, it was all practical. We all had to enrol in Business Planning on the Google Classroom. We got given an example of how to work out our hourly rate which we briefly spoke through and then we got given a plain spreadsheet with the formulas already worked out. I filled out all the figures and boxes I needed to and eventually got my hourly rate. I was surprised with my hourly rate because I had never even thought about charging anyone that much before and it's no were near what I get paid at the moment but I don't have a job in the photographic industry at the moment.

Example spreadsheet:

My first hourly rate was based on earning £25,000 a year. I then increased and decreased how much I earn a year to see how the hourly rate changed.

£20,000 a year:

£15,000 a year:

As you can see the hourly rate doesn't differ too much which I was surprised about actually. I then went on to pricing a job using another spreadsheet completed with the correct formulas. I did it based on me charging £20 an hour for my services for a 5 hour shoot:

I found this workshop really useful. I'm not yet at the stage of setting my own hourly rate and especially as a student but I now have the resources to help me when I'm at the right stage.

Cash flow planning - Start Point Finance

I wasn't really sure what cash flow was but it sounded like a good workshop to go to because it was something to do with money within a business. I took down as many notes as I could in order to help me in the future. By the end of the session I felt it wasn't the right workshop for me to go to because a lot of the people there were in their third year or doing a masters but at least I have the information now.

You can’t speak to a bank manager unless you earn over £2million

Who are they/what they do?

Commercial finance broker

Stand between clients and 90 different funding groups eg. Lloyds and Natwest

Branches don’t have bank managers anymore

Go and talk to businesses who don’t have much money or they just need some help

Paid by bank not clients

You will always have a change in cash flow

Start addressing issues as and when they come up

Set your business up and do what you want to do but you do have to think about some basic numbers

If your basic numbers don’t add up to a profit you’ll have some heartache

Need a contract between you and someone else so no confusion

Be clear about what you’re going to do and the expectation of the client and what they expect you to do

Reduce arguments later on

Help you with cash flow because if you’ve agreed they’re going to pay you in 30 days and they haven’t pid you’ve got a point without this no proof

TAX!!

Ruins cash flow

Different tax that you have to pay depending on what route you go down

Going to have to interact with an accountant or book keeper

Software that’s not much cost to update each week/day

Sage

QuickBooks

Xero

Clearbooks

Everyone will have to file their tax digitally eventually - forget paper - straight into accountancy software

Used to be a bank manager in every bank

Used to know who was who and how to help each other out

If you ask for an overdraft the bank would be taking a gamble because they don’t know if you’re going to repay it back so the more evidence you have to show that you can the better

Show what you have done and what you’re going to do and you will get given more money at a lower rate - not a gamble that way

Don’t put trust in your bank - negotiate - get an offer from elsewhere

Overdrafts

Overdrafts will give because it’s a functionality - max they want to give is £25,000

Overdraft is for cash flow movement

If you go the entire year overdraft - that’s debt

Should move onto a fixed term loan

If you’re not a homeowner and business has no assets - miss the criteria

Asset finance

If your business can afford to make payments back

If you want assets for business eg computers or vehicles - can use asset finance

Spread it over a period of time - saves you taking out a lump sum of money

Only do it on products that have a resale-able value

Invoice finance

Lowest possible interest rates

Confidential

Get insurance policy

Pre-payment is desirable - rare

Get the invoice paid before the work is done

Contractually you can force people to pay

There is legislation that the government has made to make people pay

Top things before starting out:

Tax

Accounts

Be clear about the communication to who you’re selling to and what you’re selling in a written way

There are grants and he would suggest us looking for them

Outset finance - gov sponsored - access pathway through to grant for start up businesses

Swing - SW Investment Group

Fredrick’s Foundation

Enterprise Finance Guarantee - plan needs to really good

£500-£25,000 for start up business

Cash is difficult asseting is easier

Personal Finance

FSB - Federation of Small Businesses - really good

Santander and Coop are most community minded

Comments